B2B Software Market Trends, May 2026: Valuations Stabilize & AI Breaks Records

Market Update

B2B Software Market Trends, May 2026: Valuations Stabilize & AI Breaks Records

Dedale Intelligence's B2B software market update for May 2026, covering valuation stabilisation, AI investment acceleration, data and intelligence deal activity, key M&A transactions, and Q1 2026 earnings themes for PE investors and corporate development teams

April 2026 brought the first meaningful signs of stabilization in B2B software valuations after a sustained four-month correction. The recovery was uneven, the macro environment remained complicated, and the AI investment market continued to rewrite records. This update from Dedale Intelligence covers the themes that mattered most for investors and corporate development teams in April.

Key takeaways from this edition:

EV/Sales NTM multiples for B2B software stabilized at 4.2x in April, 25% below the start of the year and well below the 10-year average of 6.6x, but the sharpest phase of the correction appears to be over

AI investment in 2026 has already surpassed the full-year 2025 total, reaching $233bn in just four months

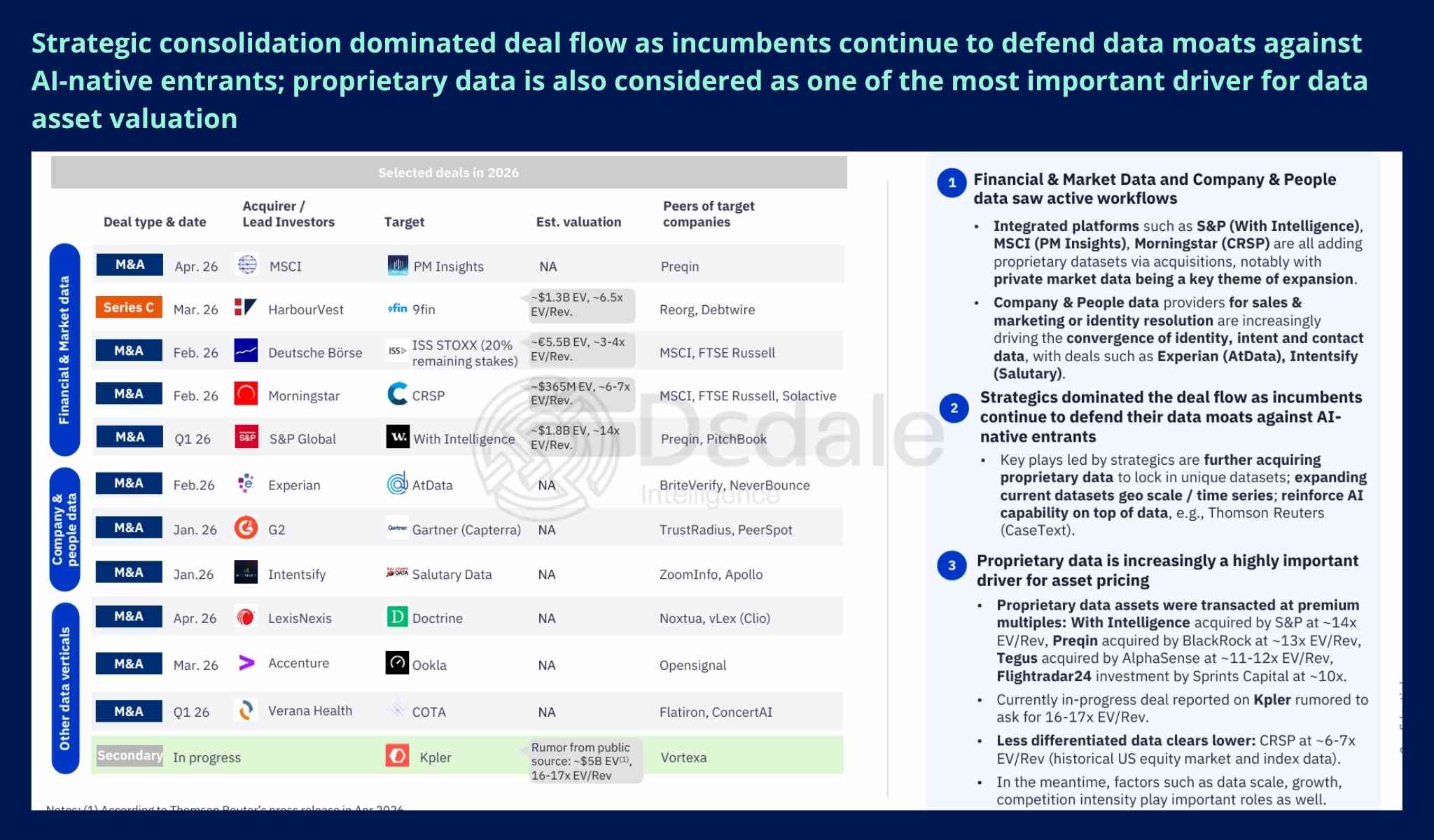

In Data and Intelligence, proprietary data is the dividing line: unique datasets transact at 10 to 14x EV/Revenue

Corporate M&A rebounded sharply in Q2 to date, lifted by the Brex (approximately €4bn) and HCSS (approximately €2bn) closes; private equity remains quiet at approximately €0.1bn

13 of 15 companies beat Q1 2026 consensus, but stock reactions split almost evenly, confirming the market rewards forward signal quality over headline beats

Valuations: First Signs of Stabilization After a Sharp Correction

The B2B Software Universe, a Dedale Intelligence index of 258 listed companies, gained 5.5% in April 2026, in line with the wider market recovery as the S&P 500 rose 10.4% and the Nasdaq surged 15.3%. The sector remains down 17.9% year-to-date, with ERP/HCM and CRM/CMS the weakest performers at -28% and -31% respectively.

EV/Sales NTM: 4.2x, down from 5.6x at start of 2026, below the 10-year average of 6.6x and at the lowest since Q1 2017

EV/EBITDA NTM: 14.9x, below the long-term average of 27.1x

High-growth companies (above 20%): 7.3x EV/Sales vs. 3.0x for low-growth

Revenue growth premium over FCF margin compressed from a peak of 77% in March 2025 to 29% in April 2026

North American software trades at 4.9x vs. 2.7x for European peers, a premium of 81%

For a look at where valuations stood one month prior, see Dedale Intelligence's April 2026 Market Trends

Source: Dedale Intelligence Analysis

Macro: Inflation Spike from the Iran Conflict, Rates Held Steady

Headline CPI surged to 3.3% in March 2026, the highest since May 2024 and a sharp jump from 2.4% in January and February, driven primarily by a 10.9% spike in energy costs following the outbreak of the Iran war. Core CPI remained more contained at 2.6%. As of Q1 2026, both the US Federal Reserve (target range 3.50 to 3.75%) and the ECB (deposit rate 2.00%) held rates unchanged at their April meetings.

Data and Intelligence: Proprietary Data Creates a Valuation Divide

AI is creatinga clear divide in the Data and Intelligence segment. Proprietary data owners, those with unique datasets built through specialist collection processes, are widening their competitive lead. Aggregators and platforms built on accessible data face growing commoditization risk as AI lowers the barrier to sourcing and structuring similar datasets. The most defensible positions combine proprietary data with workflow embeddedness, where data is integrated directly into customer operations, making switching costly regardless of competing offers.

Strategic M&A in 2026 has been dominated by incumbent platforms defending and expanding their data moats:

In Financial and Market Data, large integrated platforms are expanding proprietary datasets through acquisition, notably in private market data: S&P Global acquired With Intelligence (approximately $1.8bn, approximately 14x EV/Revenue); MSCI acquired PM Insights; Morningstar acquired CRSP (approximately $365m, 6 to 7x EV/Revenue)

In Company and People Data, vendors are converging identity, buying intent, and contact data: Experian acquired AtData; Intentsify acquired Salutary Data

LexisNexis acquired Doctrine to gain jurisdiction-specific legal data, illustrating the strategic logic of acquiring proprietary vertical datasets

Proprietary data assets transacted at 10x or above EV/Revenue (With Intelligence at approximately 14x, Preqin at approximately 13x, Tegus at approximately 11 to 12x, Flightradar24 at approximately 10x); less differentiated data cleared at 3 to 6x

From Dedale Intelligence's survey of approximately 100 financial institutions (hedge funds, private equity, asset managers, and sell-side broker-dealers):

64% plan to rationalize or consolidate their data vendor stack over the next three years

Over 60% expect to retain niche vendors alongside integrated platforms despite consolidation intent, with 26% preferring to consolidate with one single provider as much as possible

Integrated platforms showed stronger budget growth expectations (average 9.6% increase over three years) versus niche single-data-type providers (average 7.5%)

For a related view on how data integration and workflow embeddedness drive market dynamics in adjacent segments, see Dedale Intelligence's expert interview on EHS software.

Source: Dedale Intelligence Analysis

The full Data and Intelligence segment analysis, including the complete survey findings and Dedale Intelligence's competitive moat framework, is in the May 2026 Market Intelligence report. Download the full report here.

Deal Activity: Corporate M&A Rebounds, Private Equity Stays Quiet, AI Records Continue

Deal activity in Q2 2026 to date shows a divided market. Private equity remains quiet at approximately €0.1bn across 26 deals. Corporate M&A has rebounded to approximately €10bn, lifted by the Brex (approximately €4bn) and HCSS (approximately €2bn) closes. Other notable April transactions include Amadeus's €1.2bn acquisition of IDEMIA Public Security from Advent International, TPG's acquisition of Learfield at an estimated $1.8 to $2bn, and Adyen's €750m acquisition of Talon.One at 12.5x EV/Sales FY2026E.

Venture capital has normalized in Q2 at approximately €10bn across 316 deals, following the extraordinary Q1 pace driven by mega AI rounds from OpenAI (approximately €105bn), Anthropic (approximately €25bn), and xAI (approximately €17bn). Despite the normalization, 2026 YTD AI investment has already reached $233bn, surpassing the full-year 2025 total of $223bn. April saw $23.5bn invested across 125 AI deals, with three mega-deals accounting for 71% of the total: Anthropic raised $15bn in two tranches (a $10bn tranche from Alphabet and a $5bn tranche from Amazon), Ineffable Intelligence raised $1.1bn, and Firmus Technologies raised $505m. Excluding deals above $500m, the broader market recorded $6.9bn across 122 deals, the 7th highest month since 2022, with volume well above 2023 levels. The B2B software IPO window remained shut, with zero software listings despite 32 total IPOs across sectors, back in line with the long-term average.

Q1 2026 Earnings: Strong Beats, Divided Reactions, Three Structural Themes

The initial Q1 2026 earnings batch covered 15 companies in Dedale Intelligence's universe. All 15 reported year-over-year revenue growth and 13 of 15 beat consensus expectations. Stock performance split almost evenly with 8 up and 7 down on earnings day, confirming the market rewards the quality of the forward signal over the headline beat.

Key highlights from the cohort:

Amazon: total revenue of $181.5bn, up 16.6%, beating consensus by 2.5%. AWS accelerated to 28% year-on-year growth (fastest in 15 quarters) at a $150bn annualized run rate, with AI revenue at a $15bn+ run rate. Stock up 3.4%.

Microsoft: revenue of $82.9bn, up 18.3%, beating consensus by 1.8%. Microsoft Cloud revenue reached $54.5bn. AI business surpassed $37bn ARR (up 123% year-on-year). Stock down 2.6% on elevated capex of $31.9bn compressing free cash flow.

Alphabet: revenue of $109.9bn, up 21.8%, beating consensus by 2.7%. Google Cloud grew 63% to $20bn. Alphabet raised FY26 CapEx guidance to $180 to $190bn. Stock up 9.5%.

Meta: revenue of $56.3bn, up 33.1%, beating consensus by 1.4%. Stock down 8.8% on FY26 capex guidance raised to $125 to $145bn (nearly double 2025's $72.2bn actual), raising concerns about the path to returns on AI capex.

ServiceNow: revenue of $3.8bn, up 22.1%, beating consensus by 0.6%. Stock down 12.2% on FY26 operating margin guidance cut from 32% to 31.5% to absorb the $7.75bn Armis acquisition, and Q2 cRPO decelerating to 19.5%.

Planisware: stock up 11.7% as SaaS and Hosting revenue reaccelerated to 20.5%, crossing 51% of total revenue for the first time.

Manhattan Associates: cloud revenue up 24% to $117.1m, RPO reaching $2.35bn up 24%. Stock up 5.5%.

Nemetschek: revenue of $366m, up 10.7%. ARR reached approximately $1.3bn with recurring revenue at a record 95% of total. Stock up 3.7%.

AI Use Case to Watch: Workforce Management for Frontline Industries

Sona Technologies is an AI-native workforce management platform purpose-built for large frontline operators in social care, hospitality, and retail. Founded in 2021 and having raised $102m to date with 193 employees, Sona unifies scheduling, time and attendance, HR, payroll, and employee communications on a single data layer, with LLMs and an AI assistant turning real-time operational signals into staffing and labour decisions. Use cases include AI-driven scheduling, shift fill automation, AI-assisted payroll, and a manager copilot. Disruption risk is concentrated at staffing agencies, legacy HCM vendors with pre-AI architectures, and manual scheduling roles as AI handles rota generation and compliance checks across multi-site estates.

How Dedale Intelligence Tracks B2B Software Markets

Dedale Intelligence provides monthly B2B software market intelligence for private equity funds, corporate development teams, and M&A advisors across North America and Europe. The analysis in this article is drawn from the May 2026 Market Session. The full report contains detailed valuation tables, deal analysis, earnings summaries, the complete Data and Intelligence segment deep-dive, and the financial institutions survey results.

.jpg)

.jpg)